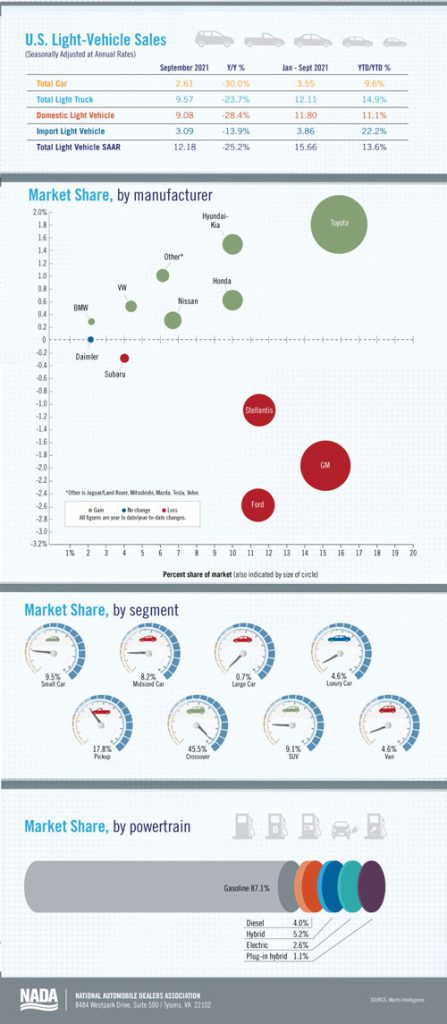

New light-vehicle sales in September 2021 fell for the fifth straight month to a SAAR of 12.2 million units. September 202l’s SAAR was the lowest since May 2020’s 12.1 million units, dropping the 2021 Q3 average SAAR to 13.3 million. Tight inventories have limited both fleet and retail sales, with fleet sales likely accounting for just 12% of total sales volume, according to J.D. Power. September 2021 started off with record-low inventory levels of 1.06 million units and will likely show little change in the final month-end data from September. Limited inventory continues to be the largest factor limiting new light-vehicle sales. Demand that would push sales rates closer to 17 million units exists in the market, but sales won’t rise significantly until inventory levels do.

Average transaction prices continue to rise in response to high consumer demand, limited vehicle availability and significantly reduced incentive spending.

Average transaction prices, says J.D. Power, are expected to top $42,800-another all-time high and the fourth straight month of average transaction prices exceeding $40,000. Meanwhile average incentive spending per unit is expected be a record-low $1,755, down $2,037 from September 2020. America’s franchised dealers are selling cars very quickly once they reach the dealership. Continuing a trend seen in recent months, the average time a new vehicle sat on a dealership lot fell to 23 days this September, down from 25 days in August and 54 days in September 2020, J.D. Power says.

According to Auto Forecast Solutions, the microchip shortage has cost the global industry 9 million-plus units of production, with a loss of 1.2 million more expected. In North America, vehicle production is down by over 2.9 million vehicles, with a further drop of 300,000 units likely. Inventory levels will probably not change much in October, and sales in fourth-quarter 2021 will continue to be pinched as the industry works its way out of the chip shortage. Because of the reduced sales pace seen in third-quarter 2021 and a dour outlook for sales and production in the fourth quarter, we have reduced our full-year 2021 sales forecast to 15.2 million units.